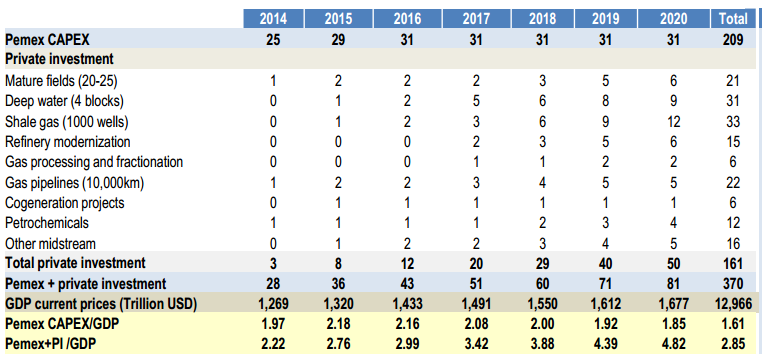

Total private investment in energy may reach $161bn between 2014 and 2020.

Mexico counting on huge private investment in energy

Beyondbrics - FT.com

Mexico’s energy reform is all about boosting investment and thus production. But the million dollar question is: just how much investment will flood in, and to what type of resource, when fields are put on the block starting from next year?

Mexico’s energy reform is all about boosting investment and thus production. But the million dollar question is: just how much investment will flood in, and to what type of resource, when fields are put on the block starting from next year?

Ernesto Marcos, a former CFO of Pemex, the Mexican state company, has hazarded what looks like the first comprehensive guess.

His estimates, which Franklin Templeton Investments publishes in a note to clients, reckon that Mexico can count on $29bn in private investment in energy in 2018, the end of the administration of Enrique Peña Nieto, equivalent to 1.9 per cent of GDP. In 2020, the investment total could be $50bn, or 3 per cent of GDP, he reckons. Total private investment in energy may reach $161bn between 2014 and 2020.

How will the investment be broken down per sector? Mexico, after all, has a wealth of opportunities, including shale plays that are the geological continuation of US formations, and deep-water riches. But shale faces significant challenges including lack of water and infrastructure, and being located in areas prone to drug cartel violence that will add security concerns. Hydrocarbons in the depths of the Gulf of Mexico will take big investment and many years to extract.

Shale, not unsurprisingly, is expected to get off to a slow start with investment of $1bn next year. But it could gather pace speedily to $3bn in 2017, $6bn in 2018, $9bn in 2019 and $12bn in 2020, when Marcos’ consultancy, Marcos & Asociados, expects it to account for more than a fifth of all private energy investment in Mexico.

Investment in deep-water prospects is also expected to hit $6bn by the end of this administration, increasing to $9bn by 2020. The slightly slower pace underscores how much of a long-term investment deep-water is.

Most investment next year is likely in mature fields and gas pipelines. Gas processing is expected to take off from 2018, while mature fields and refinery modernisations will attract some $6bn each in 2020, according to the forecast.

Here are Marcos & Asociados’ estimates in full:

Source: Franklin Templeton Investments

So with Mexico’s economy set to grow still below initial expectations – the government is forecasting 3.7 per cent for next year – just how much will all this hydrocarbons investment boost the economy?

Significantly, Franklin Templeton says:

We still do not have a macroeconomic model that will translate this additional investment into growth for the Mexican economy. However, similar experiences of liberalising the energy sector in Brazil and Colombia indicate a multiplier effect from the additional investment of at least 1:1 on GDP.

We also have to take into account that these estmates do not include additional investment from the opening up of the electricity sector. This implies that an estimate of a level of growth of another 2 per cent of GDP from 2018 onwards ould be reasonable.

Of course, Pemex, the state oil company that is losing its monopoly, will continue to be a major player: Its investment budget from 2014-2020 alone is $209bn. Put that together with private investment and Mexico’s hydrocarbons sector is expected to suck in a whopping $370bn by 2020.

Fasten your seatbelts then. Mexico’s energy sector looks like being an exciting ride.

Read the article online on beyondbrics: Mexico counting on huge private investment in energy – beyondbrics - Blogs - FT.com

No comments:

Post a Comment

Commented on MasterMetals