Bu Quoth the Raven, Seeking Alpha

The Gold Set-Up

I'm not really amused by Goldman Sachs (

GS) recently, and investors that have been taking their advice on gold shouldn't be either. Those that read my articles know that I'm a big advocate for going ultra-long both gold (

GLD) and silver (

SLV). Those that read my articles also know that I try and give people a bit of perspective by "pulling back the curtain" once in a while to show that all analysts, bloggers, and financial advisors usually have agendas.

Operating from their Keynesian-bubble on the outskirts of another dimension, Goldman Sachs reported on April 10th (merely two weeks ago) that it had downgraded its price target for gold and it advised investors to go short. As

reported by CNBC.com, Goldman analysts cited "waning" interest as a reason to not hold gold:

"Despite resurgence in euro area risk aversion and disappointing U.S. economic data, gold prices are unchanged over the past month, highlighting how conviction in holding gold is quickly waning," said Goldman Sachs analysts Damien Courvalin and Jeffrey Currie in the note.

The analysts cut their gold forecast to $1,450 per ounce for 2013 and $1,270 for 2014, the second cut in their price target this year.

On the heels of Goldman's downgrade came a barrage of headlines the following days, all of which advising that the gold "bubble" was about to burst. Subsequent to that, gold prices got absolutely demolished:

After the downgrade was issued, I penned an article on April 15th called "

Goldman's Gold Analysts Fail to Grasp Reality". In that article, I made some suggestions, saying it was not

totally out of the question for Goldman to possibly be manipulating the price of gold for them (or their clients) to buy at a lower price (bold emphasis added for the purpose of this article):

[Gold] is a non-complex issue that economists like to make sound complex in order to further their temporary need for market stimulation. Anyone that tells you that the result of Nixon shock is any more complicated than supply and demand methods learned in an ECON 101 class is trying to pull the wool over your eyes. What I mean by that is that this is a far less complicated issue than many economists will have you believe. It has to do with the amount of money in the supply versus the finite, unchangeable amount of gold available worldwide.

So, the wool that Goldman could be trying to pull over your eyes here could be the same tactics used by analysts, market makers and hedge fund traders everywhere: create a trend and buy/sell the opposite into it. If you think Goldman could not possibly be buying gold on their very own downgrade and assumed corresponding price decline, then I have some real estate in Alaska I'd like to sell you.

As I said in "

My 17 Definitive Cardinal Rules for Investing Success," you have to understand that all of these people have money in the same game they're directing the public's investments on:

As much as I hate (read: love) to bash Jim Cramer in two successive articles, he's the pinnacle example of this rule. Much of the public was absolutely flattened when they watched his interview a couple of years back on the Daily Show. In this interview, Jon Stewart played back for Cramer a YouTube video of himself openly admitting to making up and disseminating rumors about companies when his hedge fund was short them. This was the public's first glance into the dirty work that goes on behind the scenes at hedge funds; if they knew the down and dirty details, jaws would drop all the way to the ground.

The lesson I hoped the public learned from this is that 95% of the people feeding you advice; whether it's here on Seeking Alpha, on CNBC, or in the Wall Street Journal all have agendas and positions that they're trying to make money on. Believing these people disclose these positions all the time is laughable. Take everything, including what I write, as a sales pitch. Go in as a skeptic and question motives. Again, finance is a lesson in cutthroat 101.

I also noted after writing that article, that there were several (non-Goldman) analysts that seemed to feel the exact same way I did about Goldman's downgrade. In an article titled "

Should Traders Trust Anything Goldman Says?", we get another perspective on the downgrade:

"Their calls have been suspect at best, so I'm not giving this one much merit," said Jeff Kilburg of KKM Financial. "Traders out here in Chicago are not lending much credibility to their calls, because they've been so inaccurate lately."

Peter Schiff of Euro Pacific Capital goes one further. "Goldman obviously wants to buy more gold, so it needs to convince other to sell it to them," Schiff said. "It also wants to buy low, so it needs sellers to drive down the price."

I then went,

on April 15th, to comment:

The only point I can see for downgrading gold here is to be able to try and buy at a lower price. Since the Nixon shock of the early '70s, gold is only going to continue to head in one direction: up. To understand why, again, you don't need to be some seasoned analyst at a firm somewhere; you just need to understand that gold is a finite non-renewable resource with only a set limited quantity of it on earth, and printed money...well...isn't.

In addition, five days prior to me writing that article

Goldman had stated they were lowering their 2014 forecasts, as well. This wasn't just some short term correction on gold, right?

This was a major financial firm alluding to the commonfolk investors about a massive pullback in the price of gold that would run well through 2013 and into 2014:

Pointing to forecasts for stronger U.S. economic growth later this year, longtime gold bull Goldman Sachs slashed its price targets on the precious metal on Wednesday, warning prices could tumble below $1,300 an ounce by the end of 2014.

The Wall Street heavyweight not only told investors to close their long gold position, Goldman is now recommending a short COMEX gold position as one of its top trades.

"While there are risks for modest near-term upside to gold prices should U.S. growth continue to slow down, we see risks to current prices as skewed to the downside as we move through 2013," Goldman analysts Damien Courvalin and Jeffrey Currie wrote in a note to clients.

Marking Goldman's second downgrade in six weeks, the analysts cut their average 2013 gold price forecast to $1,545 from $1,610 and their 2014 average to $1,350 from $1,490. Goldman also set a $1,450 year-end target for 2013 and a $1,270 year-end target for next year.

My Reaction

Upon submitting my previous article, I was lambasted by comments and private messages, calling me everything from a conspiracy theorist to a flat out whack job. Even the Seeking Alpha editors, who remain a contributor's best friend hands down, had me tone certain things down, as they cautiously reminded me that accusing Goldman of price manipulation was a serious statement. I agreed as well, and it's important to note that I'm not pointing the finger and saying they did it, I'm merely bringing up the point that it

could have happened and I wouldn't be the least bit surprised. Anyway, I agreed, and out of respect for them and the site, toned it down a bit before subsequently being published.

I watched steadfastly, convinced that we were just in a temporary, analyst induced correction for the precious metal. Any time I would doubt that, I'd take a look at this chart I prepared for a previous article:

That sure is a lot of "corrections"! I especially love how after every one of them, we continue onward and upward. On

April 19th, nine days after Goldman's downgrade, I stuck to my guns and took a long position in another precious metal, silver. I wrote about my reasoning behind it in my article "My 5 Summer Stock Market Flings for 2013". Betting on a correction from all the bear-raid panic on precious metals, I wrote:

This is another story of putting my money where my mouth is. I've been pumping silver and gold for, well, forever. I've talked about the importance of holding gold for a number of reasons in almost every single one of my macro outlook articles that I've produced. What I recently said about gold holds very true for the same way I feel about silver.

When volatility is skyrocketing and the market is starting to pull back and correct, we should be seeing gold continue to rise in value. This correction is a major buying opportunity for people looking to hedge and firm up their investments in equities.

In an age where demand is created from the Fed injecting money into the supply and events like the horrible tragedy in Boston earlier this week are occurring on a global scale more often than ever, the security of gold is simply a no-brainer buy at these levels.

I bought SLV calls when the equity price was about $22, opposed to gold calls as a "hedge to a hedge", in essence. I hardly believe that there is a gold bubble, but what I do believe in is the possibility of other traders believing there is and causing panic. Gold is in a lot of headlines right now. Headlines mean volatility; panic buying and panic selling - this is why I'm going with silver here. Don't get me wrong, however, I'm also still ultra-bullish long term gold.

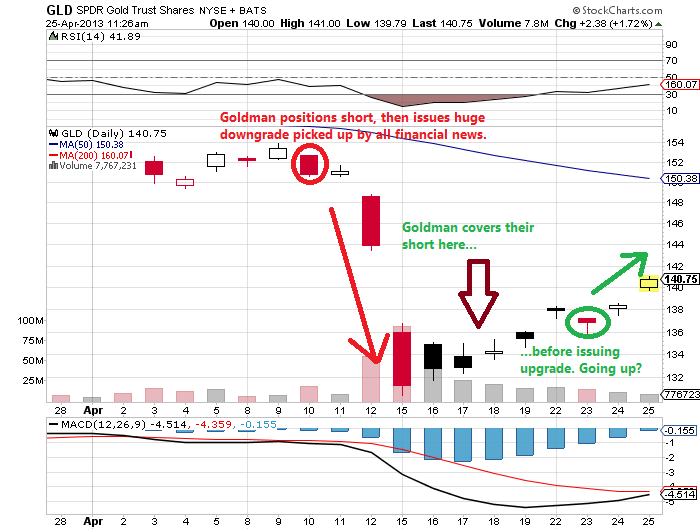

Goldman Takes a "Mulligan" that Yields Them 10%

Imagine my surprise on April 23,

less than two weeks after Goldman's massive downgrade, I see front page

on CNBC.com with the headline "

Surprise! Goldman Covers Gold Short" :

Goldman Sachs on Tuesday reversed its high-profile call to short gold, which it made two weeks ago, just before the metal sunk into bear market territory.

The firm's commodities research team said the decline in gold was more rapid than it expected, and it exited the trade with a potential gain of 10.4 percent, below its original target price of $1,450.

Interesting. Goldman was short gold before issuing a "world is going to end" style downgrade on gold and then covered their entire short after the market and the commonfolk sold off to bring gold down about 15%? Duly noted. I'm not saying its market manipulation, rather just a series of coincidences. Yeah, let's call it that.

For our visual learners, here's a picture version of all that pesky text you might not want to read through:

(Click to enlarge)

How You Can Benefit - Go Long Gold, Short or Long Term

(Click to enlarge)

How You Can Benefit - Go Long Gold, Short or Long Term

Am I the least bit surprised by any of this? Can't say that I am. I've been watching botched calls by mediums that report market activity for years now. What can you do, aside from having perspective, to make money here from gold?

Well, first, keep your friends close but your enemies closer. Know that Goldman is now holding long (again) and gold is likely to make a short term run back to the levels it was at before this whole fiasco started. It's a great time to go long gold short-term.

Long term holds will yield gains, just as they have for years now.

From the same CNBC.com article as earlier, here's confirmation that Central Banks continue to furiously stash gold in reserve:

Philip Silverman, managing director of Kingsview Management in New York, advised investors not to bet against gold last month because central bank demand remains strong. According to the World Gold Council, central banks' gold purchases in 2012 were the highest for nearly 50 years, as banks sought to diversify their reserves.

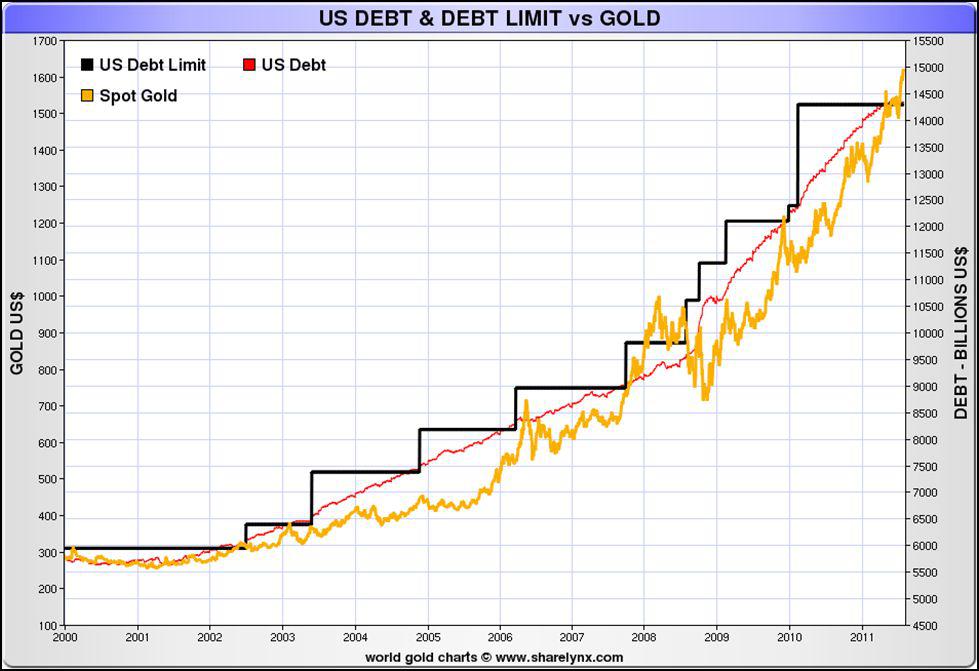

Why do you think central banks are holding it in reserve? Surely, not for some short term flip, right? Central banks know how the global economy works. You'd be hard pressed to find an analyst anywhere that could ignore yet another one of my patented "haymaker" charts like this:

(Click to enlarge)

(Click to enlarge)

Also, it's (always, in my opinion) a great time to go long for the long-term on gold. As I've consistently advocated article after article, gold going up is nothing more than the basics of supply and demand. Because we are a globe that prints money out of thin air, central banks will continue to hold gold in reserve, the corresponding price of gold will continue to rise, and you can make money on it just like the big banks.

I remain, and will remain, bullish on gold, and you should too. Best of luck to all investors.

Disclosure : Again, I am in no way accusing Goldman of blatant market manipulation, rather just pointing out things I find coincidental and trying to possibly "pull back the curtain" a bit.

I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

![[image]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_sMvhUMPbxtlldEJu-2u_zV_IeAXvsVzlAnbUEIqSUX3aPXbTF9WRNOJyePBMSTABhKU9WO0ydmjTt8XQwd8qj0e4g2-zFTDH9aXQED8ynziyouHOOUr5pYi0vIA1z65wNN96Ewbq_CVa7_9tbB8BPSxm-EUXpFWA=s0-d)

{kind=link}