Pretium Resources Inc. (PVG - TSX)

Updated Resource Sees Grade Improvement - Friday, December 20, 2013

Pretium provided an updated resource estimate for the Valley of the Kings deposit which incorporated results from the bulk sample program as well as all surface and underground drilling completed to date. Overall, the Valley of the Kings (VoK) now contains an estimated 8.7 MMoz in the M&I category averaging 17.6 g/t and 4.9 MMoz in the Inferred ounces averaging 25.6 g/, for a global resource total of 13.5 MMoz grading 19.8 g/t. This compares well with the 11.4 MMoz at 16.55 g/t in the previous resource estimate from November 2012.

While debate will continue whether the drilling and processing results from the bulk sample area are representative of the entire VoK orebody, the increase in grade and ounces in the updated resource demonstrates the reliability of the Snowden geologic model and bodes well for the upcoming feasibility study to confirm parameters of the June 2013 study. For now, we are sticking with the June 2013 feasibility parameters and are maintaining our NAV of C$24.00, a value that we believe reflects the best case upside valuation scenario for the name. Our target price of C$12.00 is based on a P/NAV multiple of 0.50x, a target multiple that accounts for the elevated level of risk associated with this intensely debated project. We maintain our Buy rating.

December 21, 2013

#Pretium Resources - Updated Resource Sees Grade Improvement

December 20, 2013

10 Top Companies Worldwide by Revenue in 2013 [#INFOGRAPHIC] #MasterEnergy

December 13, 2013

The Definitive History of #Bitcoin | @VisualCapitalist

The Definitive History of Bitcoin | Visual Capitalist

The MasterMetals Blog

December 11, 2013

#REORIENT: Morning note: #GOLD: CALL FOR YEAR END RALLY IN MINERS, THE TIME TO BE SHORT IS OVER

It's a mugs game calling gold and two years of falling prices means that even the diehard bulls have recently warned of another selloff to $1150 per ounce. For most of 2013 the bears have been out in full and analyst forecasts now range between $1050-$1250 for 2014. Not that analyst forecasts mean anything anymore as this same group had a mean forecast of $1950 for 2012 when gold peaked on the 6th of September 2011 at $1,895 per ounce. What is really interesting is that it is now consensus that gold will break below $1200 as the economic news continues to improve in the US and tapering begins. Weirdly the strong employment numbers last Friday saw gold actually trade up and continue to do so on Monday and aggressively on Tuesday. Tapering seems well and truly in the price and now somewhat irrelevant. For equity investors we talk to however it's all 'too hard' to buy the gold miners and with 10 more trading days left in the year it's difficult to find anyone prepared to nibble on the long side. But the signs are there that we won't retest $1200 and if anything gold could close well above $1300 before New Year's. A recent broker note on why Newcrest (NCM AU) should do an emergency rights issue before gold truly falls out of bed could be the classic sign that we are going up. I am not saying make a huge bet on this high cost indebted falling knife (the kind of stock you want to own at turning points) but isn't this 'rights issue' already well and truly in the price. Reassuringly Goldman's 'slam dunk sell gold' call is also proving elusive and it seems just about every broker has been falling over themselves to be the most bearish on gold - we at Reorient like to take the other side.

In short the stars are aligning for a potentially powerful move in gold miners. Short covering alone should see many of these names move 20% before real money even thinks about this trade in 2014. It could also be a long time before the pension funds come back to gold miners after so much pain has been inflicted during the 26 month selloff. However, for the early birds perhaps the equity markets are beginning to wake up to the fact that gold is now trading at a 23-25% premium in Indian Jewellery shops. Or perhaps it's watching Chinese gold imports which are now consuming between 70-100% of annual global mine supply (ex-Chinese output) depending which month you look at. Or perhaps the market is just bored of being bearish gold - 26 months is a long time.

Our bullish call on the miners we initiated on December 2nd has not yet worked but there are certainly more and more signs that it will. Copper is quietly creeping up and a close above $3.30 will be a strong signal to close your shorts and go long names like KAZ LN, 1208 HK and 805 HK. The capesize shipping rates were up another 5% today or 107% in the last two weeks. Investors malaise about the jump in Chinese coal prices as just seasonal is also a good sign. What we like most is that UK fund managers are significantly underweight the miners and are usually the first to react. The day you walk into the office in Asia and find RIO LN up 4% it's game on and that day is getting closer.

Two gold names that could see significant short covering during a gold move above $1,300 are NCM AU and 1818 HK. Don't be short the miners - you make 90% of your money in these names in 10% of the time.

Thanks, Jeremy Gray

From: REORIENT - Research

Subject: Morning note: Brownian Motion and Decoupling

December 5, 2013

#Mining in west #Africa: Where’s our cut? @Economist

Gold has long been west Africa’s dominant mineral, but iron ore is exciting more interest...From this weeks Economist.

Yet foreign companies will not find it easy. Infrastructure is poor, geological information scanty, land ownership often murky and institutions weak...

Where’s our cut?

It will be more high-tech than this

It will be more high-tech than thisThe Yekepa mine, opened in the 1950s by a Liberian-American-Swedish company, was the country’s first large-scale one. But it remained dormant throughout the civil war. In 2006, to much fanfare, it was restarted by a multinational steel company, ArcelorMittal, which has been exporting iron ore for the past two years. Other companies, such as BHP Billiton and China Union, are now active too. China Union says it expects to start shipping ore soon. Aureus Mining, a Canadian company, hopes to start producing gold in 2015. Sable Mining Africa, a British company, is the first to have secured permission from Guinea’s government to transport iron ore direct to the Liberian port at Buchanan, which is closer to Nimba than Conakry, Guinea’s capital. The company expects to begin production and start transporting iron ore in 2015.

Gold has long been west Africa’s dominant mineral, but iron ore is exciting more interest, says Rolake Akinola of Ecobank, a pan-African firm founded in Nigeria. The region is undeveloped and mining firms are busy exploring and discovering potential sites even as they develop new mines, he says. Yet foreign companies will not find it easy. Infrastructure is poor, geological information scanty, land ownership often murky and institutions weak, especially in countries like Liberia and Sierra Leone that have been ravaged by civil war and dictatorship. Commodity prices have wobbled and some big companies will be wary of investing until the legal framework is more robust.

Michael Keating of the University of Massachusetts, Boston, says that these reviews of mining codes and contracts have been instigated by Western donors who do not want local people or their governments to be ripped off. But investors may be deterred. “It’s one thing to conduct an inventory and another to go back to concessionaires and attempt to renegotiate signed contracts,” he says. “Nothing will scare investors away faster than the notion that legally signed deals can be nullified at the whim of a government agency.”

Most west African governments have signed—or pledged to sign—the Extractive Industries Transparency Initiative (EITI). The EITI tries to ensure that contracts and accounts of taxes and revenue generated by concessions are open to public scrutiny. But that is easier said than done. Last year Liberia’s government asked a British accounting firm, Moore Stephens, to carry out an audit of Liberian mining contracts signed between the middle of 2009 and the end of 2011. The audit, published last May, found that 62 of the 68 concessions ratified by Liberia’s parliament had not complied with laws and regulations. The government has yet to take action after a string of recommendations emerged from an EITI retreat in July.

Regional governments also fret over a practice known as “concession flipping”, whereby foreign mining companies that do not have the capacity to exploit sites sell their concessions to larger companies for windfall profits. “Every flip is essentially a heist on the government exchequer, with anonymous offshore firms as the getaway car,” says Leigh Baldwin of Global Witness, a London-based lobby that fights for fairer deals for local people and their governments from mining and other resources. Concession flipping, he adds, is widespread in Africa. The Africa Progress Panel, headed by Kofi Annan, a Ghanaian who once led the UN, has put out a report called “Equity in Extractives”. This, too, stresses a need for more openness in mining contracts. As people in the region demand more democracy, better deals from mining are a new priority.

Mining in west Africa: Where’s our cut? | The Economist

December 3, 2013

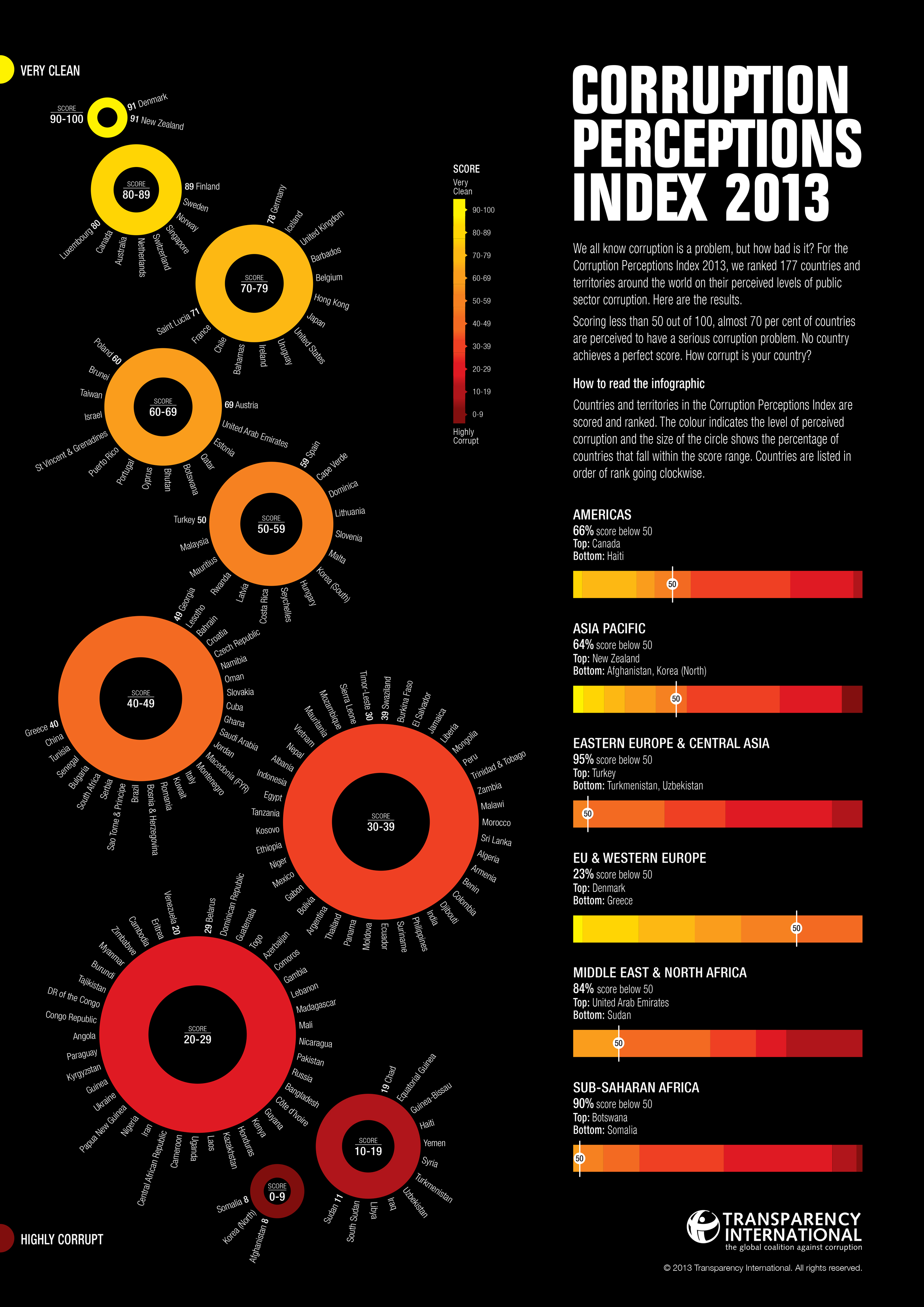

The #Corruption Perception Index 2013 - or where not to invest your money...

70% of countries scored below 50/100,

The #Corruption Perception Index 2013 - or where not to invest your money...

Master Sites

-

-

-

-

Venezuela1 week ago

-

Crude Oil Price as per July 1, 20263 weeks ago

-

-

-

-

Everyone Wants a Nanny State2 years ago

-

-

-

-

A Golden Opportunity for a Scam6 years ago

-

-

-

-

Bubbles In Several Housing Markets12 years ago

-

-

-

{kind=link}